March exhibited strong returns across major asset classes, with the recent rally propelling the S&P 500 index and several other major equity indexes to reach new all-time highs to close out the month. All major asset classes saw positive returns for the month with equities and commodities leading the way.

“In Q4 2023, 73% of S&P 500 constituents exceeded their earnings estimates2, and the index as a whole posted a 4.0% year-over-year growth in earnings. This marks the second consecutive quarter posting positive year- over-year earnings growth.”

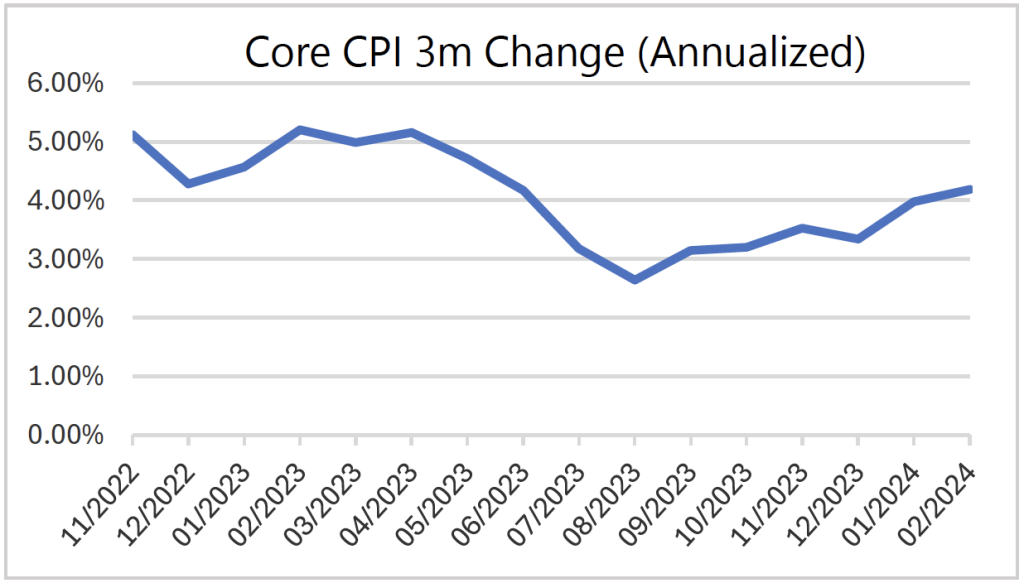

February’s inflation metrics remained relatively unchanged from the previous month. Headline CPI saw a modest increase from 3.09% to 3.15% year-over-year growth. However, PCE Core inflation, another crucial metric, saw a slight decline from 2.88% to 2.78% year-over-year. However, looking at the CPI changes over a 3-month basis reveals a less optimistic picture, with a steadily increasing trend of costs beginning to rise again. This data suggests rate cuts may come later than anticipated.

On March 20th, the second FOMC meeting of 2024 took place, with the federal funds rate remaining at 5.25-5.50% for the fifth consecutive meeting. The Fed reiterated their stance on not reducing rates until inflation reaches a sustainable 2% target. The release of the Summary of Economic Projections (SEP), which occurs quarterly, provided insight into FOMC members’ projections on GDP, inflation, unemployment, and the Federal Funds rate path. The median projections for the federal funds rate remained unchanged for December 2024, with approximately three 25 bps rate cuts expected [1]. However, projections for later periods have become more hawkish, with the federal funds rate projected to decline to just 3.90% for December 20251. Furthermore, projections for real GDP were revised upward, and the unemployment rate was slightly lowered, indicating a belief that the economy may remain stronger than originally anticipated. This optimism of economic resilience was supported by the recent upward revisions in Real GDP growth for Q4 2023 to 3.4% year-over-year growth.

Additionally, the ISM Manufacturing PMI, a diffusion index (where a reading below 50 indicates contraction), has finally crossed above the 50 threshold for the first time since October 2022, marking a positive shift and serving as an encouraging leading economic indicator. However, the ISM services PMI has continued its downward trajectory and both the Manufacturing and Services PMI do remain well below their 10-year averages.

As we conclude the first quarter of 2024, equity markets have showcased strong resilience across the large and mid cap equity sectors, with the S&P 500 index reaching all- time highs in both February and again in March, reaching 5254.35 as of quarter-end. These impressive returns have occurred alongside a rise in the 10-year Treasury yield, which began the year at 3.88% and rose by 32 basis points to 4.2% by the end of the first quarter. The equity rally and recent momentum has been fueled by a robust earnings season that has exceeded expectations. In Q4 2023, 73% of S&P 500 constituents exceeded their earnings estimates [2], and the index as a whole posted a 4.0% year-over-year growth in earnings. This marks the second consecutive quarter posting positive year-over-year earnings growth. Most notably, communication services emerged as the leading sector with a growth rate of 45%. The S&P 500’s forward P/E ratio now stands at 21.84 at the end of March, significantly higher than the 10-year average of approximately 17.7 [3], suggesting that the market is pricing in relatively minimal risk and holds optimistic expectations for companies’ growth prospects moving forward. The well-known Artificial Intelligence (AI) theme has continued to contribute to much of the optimism in the equities market with 179 S&P 500 companies citing “AI” on earnings calls [4]. Ultimately, only time will reveal the validity of the unfolding AI narrative and the extent to which efficiencies derived from AI technologies will translate into tangible realized earnings growth for companies.

- https://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20240320.pdf

- https://insight.factset.com/earnings-insight-infographic-q4-2023-by-the-numbers

- https://insight.factset.com/sp-500-earnings-season-update-february-16-2024

- https://insight.factset.com/second-highest-number-of-sp-500-companies-citing-ai

Download The Full Market Update

~Diligently Yours,

Your Smarter Way Portfolio Management Team

Please note this is for information purposes only and should not be construed as investment advice or recommendations made by A Smarter Way to Invest. Please contact your Advisor if you have any questions about this market update report or if you would like to discuss your personal financial situation in more detail.